An Exchange Traded Fund is a great investment. In this guide we discus what an ETF is, what factors you should consider when investing in one and the key terminology you will encounter. By the end of this guide, you’ll be able to pick the perfect ETF to meet your investment goals.

What is an ETF?

ETFs are Exchange Traded Funds – investment funds that trade on a stock exchange.

ETFs are selections of securities. When you buy an ETF, you buy into a broad collection of investments. They are often a simple and cost efficient solution to investing, enabling people to gain access to diverse investments with a low overhead and low initial investment.

ETFs are available to buy through almost all brokers, and you can buy them in a stocks and shares ISA. You can buy and sell an ETF just like you would do an individual stock. As they are traded on the stock market, you can buy and sell the at any time of day – as long as the exchange the ETF is listen on is open.

Why Should I Invest in an ETF?

If you pick the perfect ETF, you will have selected a low cost, well diversified investment.

ETFs make investing simple. You can easily pick a single ETF and have global diversity within your portfolio. Diversity is a great way to reduce overall risk and ensure a fall in any given sector, region or specific company does not impact your investment too much.

ETFs are often very cheap. The ongoing costs for a global ETF such as the Amundi Prime Global can be as little as 0.05%.

Factors to Consider When Choosing an ETF

ETFs are exceedingly popular and hence there are many options available. When looking to pick the perfect ETF for you, the following should be key factors.

Index

The majority of ETFs will track a given index. This could be something like the MSCI world index, a country index such as the FTSE 100, or a sector index like the NASDAQ Global Semiconductor Index.

All of these indices are constructed in different ways to track different areas of the market. Picking a specialised index could well see your investment be much more volatile compared with a well diversified ETF.

Remember that past performance of an index does not guarantee future performance.

Active vs Passive

Whilst many EFTs will be passively tracking the selected index, some will be actively managed. Actively managed funds aim to beat the index by using the knowledge and experience of a fund manager. Often these ETFs will cost a little more as we have to pay for this active management.

Whilst active management sounds positive, Morningstar conducted a review and found that in 2023 passive funds outperformed actively managed funds.

Tracking Error

No ETF can track an index perfectly, hence every ETF will have a tracking error based on the index itself. In some cases this error can work in your favour, in others it can work against you.

Most tracking errors come down to sampling or replication methods so it’s best to use a tool such as JustETF’s Fund Screener to see the real impact. Often for the large ETFs the tracking error is fairly small.

Distributing or Accumulating

Many stocks will offer dividends. This is a payment made by the company to the shareholders. If you invest in an ETF, the ETF will pay these dividends out.

This payment can be made in two ways. Either paid directly to you as a holder of the ETF, this is distributing. Alternatively the dividends can be reinvested into the ETF and upping the value, thus accumulating.

Many ETFs offer both formats. Receiving dividends can be a nice bonus, but if you are simply going to reinvest dividends than an accumulating fund is likely to be the best option as otherwise you’ll have to manually reinvest or potentially pay to reinvest.

Cost

Often referred to as the Ongoing Cost Figure (OCF) or Total Expense Ration (TER) these are the ongoing costs for the ETF. These are expressed as a percentage so a 1% TER on a £100 investment would be a cost of £1.

It’s important to not that there may be other fees associated with an ETF such as additional management charges, entry or exit charges or a big spread on the price to buy into an ETF vs sell it.

Every broker will provide a link to the factsheet for the ETF which will list all the fees you’ll incur such as this one for

Liquidity

Illiquid assets will be harder to buy and harder to sell. Simply, with fewer people interested in an ETF you may have to wait longer to both buy and sell the ETF.

As a result, it’s often best to pick large ETFs with a fund size of a few £100m. This should ensure a sensible spread between buy and sell prices and mean that when the time comes to sell there should be plenty of people wanting to buy.

Currency

When buying an ETF it’s important to know what currency it trades in. If an ETF is listed in a foreign currency you will have to pay a foreign exchange fee when trading in and when trading back out.

Some ETFs will be listed in multiple currencies on the same stock exchange, so make sure you pick the one listed in your currency!

Whilst many EFTs will be listed under different currencies, the underlying assets will be held in another. For most global ETFs you’ll find they may be listed in GBP but the underlying currency is USD. As a result, as the exchange rate between GBP and USD varies so do your returns from the ETF. It may well be that the underlying index goes up by 1% but you only see a 0.5% change because of the exchange rate varying.

To overcome exchange rate volatility you can buy hedged funds. These ETFs operate in exactly the same way as an unhedged fund, except there are currency agreements in place such that you won’t be impacted by exchange rate changes. This can be good and bad. For UK investors if the USD increases against GBP then you’ll gain more, so sometimes the currency hedge can mean you lose out.

Replication Method

ETFs can replicate an index in a few ways. Some funds will 1:1 replicate an index. Often larger funds will physically sample an index. They’ll own most of the assets but not all of them. When managing 4k+ assets with some making up on a fraction of a percent of the index these are often skipped to help reduce costs.

Some EFTs will operate a swap method. In these cases the fund doesn’t own the underlying assets however does receive the returns and dividends. They have an agreement in place with the entity owning the assets. These funds often incur an additional swap fee which will be listed on the key information document. They are however exempt from withholding tax which will help returns.

Domicile

We’ve talked about withholding tax and the need to complete a W-8BEN form previously. Just as individuals may have to pay additional taxes, so to the ETFs themselves.

The key thing to note here is that where the ETF is domiciled makes a difference. You can find this on the key information document, and most brokers make this clear when browsing ETFs.

For UK investors, we recommend looking for ETFs domiciled in Ireland as these only pay 15% withholding tax compared with 30% for Luxembourg. Note this tax only applied to physically replicated ETFs.

How to Pick The Perfect ETF

Whilst you may be able to get great information from a broker, it can often be best to go to the ETF providers website directly. Here you’ll often find more detailed information, the full list of holdings and be able to find out if the same ETF is listed in a different location. FWRG for example – an Invesco All World ETF, is explained in detail on Invesco’s website along with the other listings for the same underlying fund. Here you can see the ETF is also listed on the London Stock Exchange in USD under FWRA.

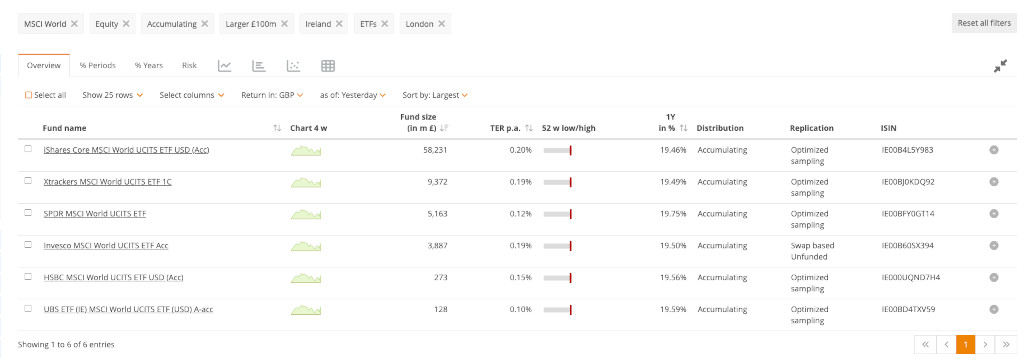

I highly recommend using a tool such as JustETF’s ETF Screener. Here you can find ETFs meeting your requirements. For example you can see all ETFs matching the following criteria:

- Tracking the MSCI World Index

- Listed on the London Stock Exchange

- Domiciled in Ireland

- Accumulating

- Over a £100m in the fund

Common Pitfalls

Picking an ETF can be a complicated process. There are some common mistakes or pitfalls people make when picking an ETF.

Ignoring Fees and Costs

By far the most common mistake it ignoring the fees and costs associated with an ETF.

We’ve talked about how stocks and shares investing is safer over the long term. As such, we should consider the impact of fees over the long term. Picking at ETF with an ongoing fee of 0.1% vs 0.5% doesn’t seem like a big difference over the course of a year. Multiply that over the course of a 20 year investing horizon however and the costs really add up.

Consider a £10,000 investment with an approximate 10% rate of return – not unrealistic for the S&P 500. With a 0.1% fee, after 20 years you’ll have £71,841. With a 0.5% fee, this reduces to £66,360. That means you miss out on £5,481 for picking a more expensive ETF!

Focussing Solely on Past Performance

We’ve all heard the phrase past performance does not guarantee future performance. Just because an ETF has performed well in the past does not mean that will continue.

Sector based ETFs could be very cyclical. Recessions will not impact all companies equally. Often recessions can be associated with poor performance from the finance industry as interest rates are lower. However, consumer staples such as food may hold value in a recession.

Other sectors can have big booms, such as the current AI boom driving semiconductor stocks like Nvidia sky high.

Not Rebalancing Your Portfolio

It’s easy to overlook rebalancing your portfolio. Rebalancing may come at a cost, particularly if you have to sell some equity to buy other equity. Doing so will incur costs on the spread, the difference between the buy and sell prices. You’ll pay more to buy than you’ll get from selling.

Leaving a portfolio unchecked however will mean that it will become imbalanced. Should a particular area of your portfolio do well, that will shift the balance of your investments. That may be something you are comfortable with, however you may prefer to semi-regularly rebalance your portfolio to ensure you remain in line with your investment strategy.

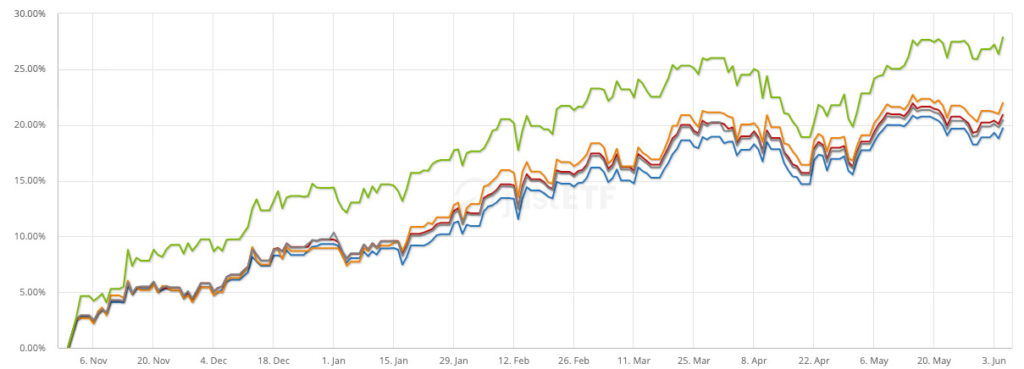

Did I Pick the Perfect ETF?

I’ve previously talked about how I picked the best stocks and shares ISA for me. After much research I picked a selection of ETFs to meet my overall investing goals of:

- Learning about the stock market

- Growing my wealth

To accomplish this I split my portfolio into a three main groups:

Global ETF

A large portion of my total investment has gone into a global, developed world ETF. This ticks the boxes for the lower end of the spectrum in terms of risk, a low cost and a big name provider with lots of liquidity.

It’s an accumulating fund so I don’t have to worry about dividend reinvestment and it’s in GBP so no foreign exchange fees. It’s a developed fund, so doesn’t cover emerging markets however I’m comfortable with this choice as it’s cheaper than an all world fund.

A Collection of Regional ETFs

In a bit of an experiment I selected a handful of regional ETFs to make my own equivalent of a global ETF. Platforms such as Trading 212 make it easy to create investment pies so you can set weighting for a number of investments and then invest in the pie itself. This makes it really simple to invest based on your chosen weightings and they also offer a simple one button rebalance process.

My intention here was to allocate a small portion of my funds to see if I could replicate the performance of the global ETF but with overall cheaper fees. This also enabled me to change the weightings on regions I believed would be up and coming compared with the global ETF weights.

It’s fairly straight forward to cut fees significantly with this approach – the USA makes up 60%+ of most global ETFs, but costs for a common USA index, the S&P 500 often come in around 0.05% – significantly below the 0.15-0.25% you’d likely pay for a global fund. There are of course many downsides to this approach as you need to keep on top of rebalancing which a global ETF would do for you.

Thematic ETFs

I also allocated a small portion of funds to a couple of popular thematic ETFs to see how they compare vs a global index. Defense, semiconductors and uranium. We’ll see how they do, but I expect them to be more volatile compared with the global ETF.

Conclusion

For most people a single accumulating global ETF that you can regularly invest into will likely be the the most straightforward option, and probably provide the best returns. That is why the majority of my funds are in global ETFs. I’ve just decided to experiment a little with a small portion of my portfolio.